Understanding transfer duty

Transfer duty is a tax levied on the value of any property acquired by any person by any means. So, whether you buy a property from a seller or acquire it in any other way, you will have to pay SARS the tax due. There are exceptions to this rule which are discussed below.

According to SARS: "For the purpose of transfer duty, property means land and fixtures and includes real rights in land, rights to minerals, a share or interest in a residential property company or a share in a share-block company."

Transfer duty should not be confused with the property transfer costs. Property transfer costs are the fees paid to the conveyancing attorney who attends to the property transfer from seller to buyer, whereas transfer duty is a tax payable to SARS.

Rate of tax

Transfer duty is only payable on the transfer of properties valued at more than R1 million. If the property you are buying is worth less than R1m, you will not be liable for transfer duty. However, you will still have to pay transfer costs to the conveyancer.

If the property you are buying is worth more than R1m, you will only be liable for transfer duty on the amount above R1m.

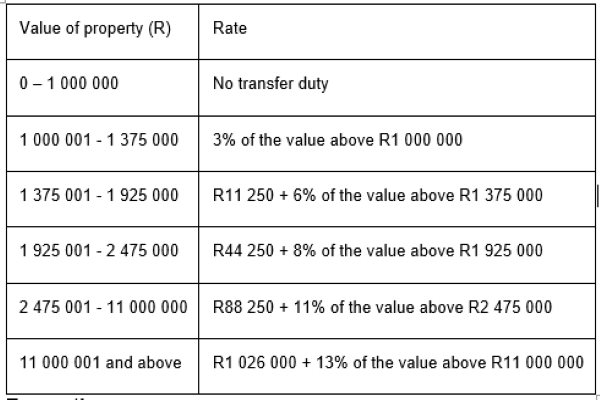

Transfer duty is payable within six months of the date of acquisition of the property, and failure to make payment timeously will result in penalties. However, the conveyancing attorney responsible for transferring the property into your name will usually deal with this. SARS issues transfer duty tables each year, with details of the amounts due on the transfer of properties of different values.

These are the transfer duty rates applicable from March 2022 to February 2023.

Exemptions

Property transfers are exempt from transfer duty in the following circumstances:

Marriage in community of property. If a property owner gets married in community of property, their spouse automatically becomes the owner of a half-share of the property without needing to pay any transfer duty.

Divorce. Transfer duty does not apply where a property is awarded to a spouse in terms of a divorce order. This exemption applies to all marital regimes as well as civil unions. However, if the property is not awarded to a spouse in terms of a divorce order and the parties reach an agreement outside of the formal divorce proceedings, the spouse who acquires the property will be liable for transfer duty as well as any transfer costs payable to the conveyancers.

Inheritance. Beneficiaries and heirs are exempt from paying transfer duty on property they inherit from a deceased estate. This is regardless of the nature of their relationship with the deceased and irrespective of whether or not the deceased died intestate (without a valid will). In this instance, heirs and beneficiaries still need to pay the conveyancing attorney's costs of transferring the property into their name.

Cancelled transactions. If the purchase of a property is cancelled before the transfer is registered at the deeds office, there will be no liability for transfer duty. The provision is that SARS must be satisfied that the cancellation is legitimate.

VAT

Developers usually offer homes for sale in new developments with no transfer duty payable - irrespective of the property's value. Instead, buyers pay Value Added Tax (VAT) on these homes, but this is usually included in the purchase price of the unit.

By law, a transaction may not be subject to both VAT and transfer duty. However, when it comes to property transactions, the payment of VAT will always take precedence over that of transfer duty, where the seller - usually a developer - is a VAT vendor.

When you buy a property, check to see if the sellers are registered for VAT. If they are, then VAT will be payable on the property purchase and not transfer duty.

Budget

Transfer duty and property transfer fees are additional costs you need to budget for when buying a home. Be sure your finances are in order, and don't be caught unawares.

Author Sarah-Jane Meyer